Founded in 2004, and with offices in South Africa, the UK and the USA, Westbrooke is a multi-asset, multi-strategy manager of alternative investment funds and co-investment platforms. Our purpose is to preserve and compound our clients’ wealth to cement their future prosperity.

MORE ABOUT US

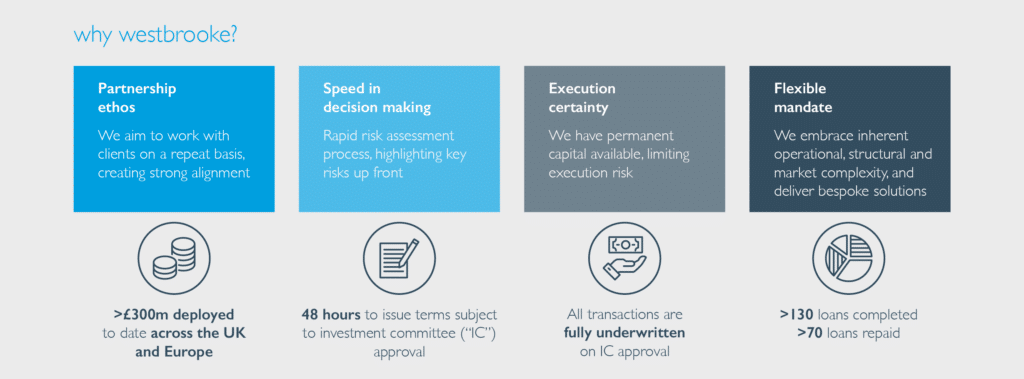

why westbrooke?

A team of highly experienced professionals with decades of investment experience

Core investment philosophy focused on the preservation of investor capital and compounding returns

Heritage as a shareholder and operator of assets

Financial alignment – invested materially alongside our clients and partners

Providing a unique gateway to alternative investment opportunities which are traditionally difficult to access

MEET OUR TEAM

why alternative investments?

Since alternatives are generally uncorrelated to typical equity and bond investments, investing in them as a core component of a portfolio may provide broader diversification, reduce risk, reduce volatility and enhance returns.

LEARN MORE

latest news

Westbrooke Alternative Asset Management is pleased to announce it has concluded a R70 million NAV finance facility to an established South African private investment holding company, to facilitate the exit of a consortium of minority shareholders. The loan, underpinned by

read more

Westbrooke Alternative Asset Management UK has collaborated with Trimountain Partners to provide a significant investment into one of the fastest-growing parking management solutions and service providers in the UK, Horizon Parking. Headquartered in Chelmsford, Horizon Parking provides integrated end-to-end parking

read more

Head of South African Capital Solutions for Westbrooke Alternative Asset Management, Jonti Osher, discusses the investments Westbrooke has made over FY24 into Solar PV projects through the Westbrooke Renewable Energy Alternatives (Westbrooke Real). Classic Business on Fine Music Radio with

read more

stay in the know

Complete your details below to sign up for the latest Westbrooke investment local & offshore news & opportunities!

KEEP ME INFORMED